Note that there are 2 F&Ns. 1 is listed in Singapore, the other in Malaysia. The one I am talking about is F&N Malaysia which has its operations mainly in Malaysia and dairy products in Thailand. F&N Singapore, the holding is much bigger and both are just as well run.

All the good things will not come to an end but one very significant factor will derail F&N's competitive advantage for quite a while. What is that?

The Coca-cola company factor

Once a good partner, now a major nemesis in Malaysia. Why is that? F&N used to be the bottler for Coke - for more than 50 years remained that way. When Coca-cola was just happy with building its Cola range and maybe Sprite's market share in every country that it goes to, F&N of course was just as happy being the bottler. Along the way, F&N used the partnership and distribution strength it has built in Malaysia to introduce several drinks of its own brand. Hence, we in Malaysia are introduced with 100Plus, F&N carbonated drinks, Seasons and several other brands - all owned by F&N. Problem is that Coca-cola has the same flavoured drinks. But F&N doing the bottling and distribution so well and Coke, the marketing master was still growing at a nice pace that both were happy with this arrangement for a while. Until both Coca-cola and Pepsi realized that they cannot just rely on carbonated drinks for growth as they are not growing as much anymore as before.

Hence the multi-drink strategy. To have a multi-drink strategy, you will need a multi-marketing strategy and to be able to test out the market for acceptance of any new drinks that they introduce. F&N with its own brands are just not going to do that. Imagine they are bottling for Fanta, Minute Maid while F&N is also selling its own brand of similar range. Surely, Coca-cola being the tai koh (big brother) is not going to allow that as well. Malaysians who do not know, Coca-cola actually has over 100 types of drinks, just that they are not here - yet.

All good things came to an end in 1 September 2011. In fact, the termination was announced much earlier - sometime in 2009 but it took Coca-cola more than 2 years to build its plant in Nilai and together it has to build a distribution channel as well. Remember, Coca-cola did not need to worry about that when F&N was doing the hard work for them.

Good marketing however, is much tougher than good distribution. Coca-cola, is not what it is today (and made Warren Buffett very rich) if not for it being the best marketing company in the world. Apple took over that realm for last 10 years I should say.

Just look at all the strategic shelf space it took over the last year. It has the might. And some time around last year, Fanta (owned by Coca-cola) was brought back. I foresee Coca-cola is not going to stop there having built a 30 acre plant. It will be fighting for market share in the sports drink market and everything else it can make from selling water.

From that, the Malaysian soft drink market is to have 3 major players - Coca-cola, PepsiCo and over time I foresee F&N will drop to be that 3rd player.

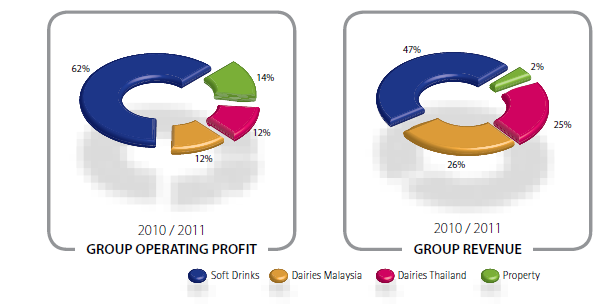

So what is the effect to F&N? Tremendous if you look at the contributions the soft drink business brought to them.

|

| Blue Color shows the contribution from soft drink to F&N in FY2011 (30 Sep) |

Operating Profit from soft drinks dropped more than one fold (RM88.36 million to RM41.17 million) . Note that the drop in dairy business in Thailand may be short term though due to massive flood last October - November around Bangkok.

I believe this one quarter impact is not a short term thing. It is going to be a long fight for F&N - one that may turn out to be a big headache for F&N.

Hence, at the current price of RM18.18 valuing F&N Malaysia at more than RM6.56 billion and over 20x FY2011's profit - I think is going to be tough for F&N to maintain in near future. No major property project or any immediate diversification is going to change the immediate loss from Coke's business so soon.

Note: The theme for F&N's Annual Report last year was "Sustainability through Diversity" - hence, you can already guess what they are thinking!

Happy Investing!

visit www.fb.com/MalaysianInvest

12 comments:

Don't forget the following,

1) Overseas expansion of softdrinks sales, i.e Thailand, Middle East which may well cover the loss in Malaysia to Coca Cola

2) Increase capacity of Dairies Malaysia.

3) Loss in Dairies Thailand is one off and claimable.

4)Property development in the old PJ area.

Taken Note. But expansion, they could have done it years before be it to Thailand and Middle East. They knew the Coca-cola franchise was for them to lose years before. If the expansion is to be realized probably would be from the Singapore listed coy.

Property development in PJ is one off. If you look at Frasers Park in Loke Yew, they took profit after completion of development - it is not like they have taken up property management. I am not discounting the work they have done as a property developer but to cover the Coke franchise lost - tough.

I did say losses from Dairies in Thailand is one off. F&N is still a good company but to return to that profit level in FY2011 - tough unless they recognized a one off profit in Seksyen 13.

Expansion - Not able to execute then due to contract binding with Coke i.e they are not allowed to sell any of their products other than Mal and Sgp as long as the contract is enforced. Also, take note that it is F&N who requested for the contract to be terminated and not the other way round as they forsee the limitation in their sales in Malaysia.

Expansion will be from Sing - agreed ( as recently announced the establishment of Fraser Indonesia) but Thailand itself is a huge market for F&N Malaysia.

Property- They have reiterated that they are not focus in Property. That's why they've partnered with Fraser Sgp to develop the land over the next 10 years.

One off profit - yes and it will be above 100 mil this year both from the sale of land (RM 50 mil) and the halal hub status(75 mil?).

This is a turning point for F&N currently. Make or break. They can soar like an eagle if successful regionally. Otherwise, they will be beaten down to their knees with the rising competition by coke and the escalating cost of raw material of sugar in particular.

Great comment and a good heads up on the one off profit.

On the termination of the bottling contract, I think both parties F&N and Coke would like to have their angle of the stories. But if you look at the global strategies both Coke and Pepsi have engaged - they are buying back most of the bottlers starting from 2009. In fact Pepsi started that first - 1 year later Coke followed suit.

I am not worried over the escalating raw material costs as in most strong brands, they will be able to find ways to pass to us consumers. :(

Most consumer retail stocks have not been affected much by inflation last 2 years.

Perhaps the best way to counter the competition is to sell 100 plus to 100+ countries including the US and China. If Mao were only to defend Kuo Min Dang in a few provinces, and dared not venture to other provinces especially the north eastern of China, communists would not have come to power in China. I always believe that a good product will always cut a slice of market share from another good product. Just like almost every great star has fans.

I am very sure so I should have removed the word "almost" from my previous post.

Kirin offer to buy F&N Malaysia

That is F&N Singapore, not F&N Malaysia.

Like I said in my article, F&N Spore is different from F&N Malaysia.

Kirin is offering to buy the Malaysia operations from Fraser and Neave Singapore for the soft drinks and dairies. http://www.btimes.com.my/Current_News/BTIMES/articles/20120726142724/Article/index_html

If Kirin buys F&N Malaysia, it is even better, but lets see how it turns out

Now, Coca Cola is also interested to buy F&N Malaysia!

A good move actually as if F&N is up for offer, Coke will want F&N's soft drink business more to eliminate competition.

At current price, or higher I think F&N will sell but the so many suitors actually suite Coke and rest. Heineken will not want the soft drink business. Similarly, Coke will not want the beer brewing business.

Post a Comment