A few friends and I were discussing about this and the news came as a surprise as we thought that the RF division of Broadcom or rather then Avago is the cashcow for Broadcom. It is the business unit that enables Avago and its CEO to where it is today. Ask any veteran in the business, when HP split into 3 companies, it was the wireless division which was the one harder to bring up. Of course things changed when Apple introduced Iphone 3 and Avago's filters were monopolizing the industry which later on includes selling the chips to Androids phones.

Anyway, could the news be true as Broadcom has not made any statement. Today's Broadcom is much much more than the old Avago which was barely a $5 billion company. It has so many cashcows and who would want to bet against one of the best fund manager who is also the CEO of Broadcom aka Hock Tan. Broadcom today is building solutions for the cloud which includes semiconductors for servers and it is expanding into software, hence the acquisition of CA and Symantec's enterprise division, a security company. These happened after its much talked about failure to acquire Qualcomm. If that would have happened, the industry would be amazed. I would have been proud of a Malaysian who probably would have been one of the best manager in the recent semiconductor industry.

We also talked about the today's Broadcom or Avago. We hear and know that it is not a visionary company. It is a company that has proven to be able to pick up technologies which has great potentials for the next medium term and make them even more profitable. Those traits has been proven in its deals with LSI Logic, Brocade and ultimately Broadcom itself - through a takeover by Avago. In short, Hock Tan and his team are great deal-makers, executioners, managers and negotiators. On the bad side, they do not really take any deal with a passion. Cutting costs is part of the game - and that involves cutting people. The plan to sell the RF division is one of such, it was its saviour. Now it is not needed anymore. Why? The acquisitions of CA and Symantec have increased Broadcom's debt to exceed $30 billion against its cash of $5 billion.

While Broadcom has great cashflows, it however will want to do something before it can do another deal. Hence, it needs to sell before it can buy big again. Hence, the plan to sell the RF division. Anyway, for the next generation 5G technology, Broadcom's RF may not be at a huge advantage anymore. Several new companies are moving big into it, and it is ripe time to sell. Remember, Broadcom is not that much of a technology visionary but a company which manages its technology dominance very well.

What then will happen to Inari? For those who may not know, the RF business is huge for Inari as compared to its other businesses. It is also probably more profitable. Will Inari continue to still obtain jobs from its new acquirer assuming the business is sold. I would not want to make a guess. However, one thing I can be quite certain is that the relationship would not be the same. One must remember, it was Broadcom which gave opportunities to Inari back in 2006 (around) when Avago then wanted to focus on being a factory-less company. It was looking for companies or entrepreneurs to take over the manufacturing (packaging) business. In fact, at one point of time, Avago was a shareholder of Inari prior to its listings.

The industry knows the relationship between Broadcom and Inari. Will Broadcom give Inari business from its other product line? That is up to Inari to prove itself. One thing as well is that the age of important decision makers from Broadcom which provides the opportunities for Inari is not so bright for Inari's future as they have reached (or almost) retirement age.

The way I look at it, with the share price of Inari trading at 30x PE (after the recent drop) and given that the future is uncertain - it does not look too good. Even if the division is not sold, this news bring reminders to us. A 30x PER which equates to 30 year to get back your money does not provide a good comfort, given the pace of the industry move. Inari will definitely be there but it has to look for other deals which may not be as lucrative but to grow.

My worry is that the cradling stage for the largest Malaysian semiconductor company - by market cap - may be over soon and it has to look after itself and it may not have the strength to do so - if you know what I mean.

Saturday, December 21, 2019

Tuesday, November 26, 2019

Subscribed for WCEHB-PA and WCEHB-WF

Due to the fund raising exercise from WCEHB, I have subscribed for all including excess as I have 67,200 units of WCEHB.

In the end, I now have 136,000 WCEHB-PA and 34,000 of WCEHB-WF.

The position is as below.

I intend to convert the RCPS into WCEHB in future within the first year.

In the end, I now have 136,000 WCEHB-PA and 34,000 of WCEHB-WF.

The position is as below.

|

| Click to enlarge |

Sunday, November 24, 2019

Where are our stocks heading? What should our focus be now. Part 2

The government today is pushing hard on automation and investments while reducing unskilled foreign labor although the strategy may not bear as much fruit for the moment.

Why is the government doing this? Before we go deep into the sectors and where should the growth be in Malaysia, let's look at the components of growth in the perspective of Malaysia and where should our focus be.

Let me put the context of economic growth to a simple 4 portions

Consumption basically depends on the economic strength of the country and also how fast the velocity of the money flows. As a country we have been increasing and to a certain extent dependence on local Consumption for much part of our growth in the last 15 years. One can see through the strength of private consumption, so much so that our private debt to GDP exceeded 80% for quite a number of years now.

Investment (I) refers to in this case corporate private investor invests into the country. They may be foreign or local investor. One trend that we see nowadays is the public-private investment (PPI) initiatives as government will not be able to afford to invest and manage those projects themselves alone. Through an agency such as MIDA, we have also been encouraging foreign investments besides local.

Government (G) is where we see the expenditure of the government both in operational and capital expenditure. Both operational and capital are important as operational is where government employees' remunerations are paid as a consumer as well while developmental expenditure and mainly the investments which are made by government rather than private sectors. Examples of developmental expenditure are building of schools, hospitals, roads.

Lastly, the component of Exports (X) and Imports (M) which is highly relevant for a trading country like Malaysia. For certain industry, Import and Export goes hand in hand. Example trading industry. If there are no value add, then we are merely acting as traders. We import and export the same product. When there are value add for example, buying semiconductor components, materials - enhance them - we export them back into finished goods or more developed components. A strong country will be able to sell services as exports for example Intellectual Properties.

From the above, countries will work on various components in coordination among various departments, ministries. At different stages each country would develop their different components on various speed and level. Example, in the 1950s, US was pretty strong as an export country. Today, it is very a country doing much more Imports. China was such during its developmental years from 1980s until now. Recently, the internal policies have also been developing local consumption.

How do those four segments above interlinked. They are Vastly and Highly interlinked. Without investments for example, be it local or foreign, the Exports component will not be strong eventually. Without investments in ports, roads for example, there would not be further investments in trading, transportation, factories, housing.

Without strength in investments and Exports and Imports, we would not be able to grow our consumption. Malaysia was developing our local consumption sector post financial crisis in 1998/99. The velocity of the consumption will also create more consumption. However, for a country which is limited by its per capita income at a developing nation level, to grow consumption without focus on other components, higher debt will kick in. Too much debt is a problem as we have seen the collapse of the sub-prime housing crisis in US.

Malaysia is now at a stage where consumption is at its high while local private investments (non-GLCs) is tapering for some time now. We need to readjust. There is a need for more local private and foreign investments to promote strength in other segments.

I see that the government is aware of the above sporadically but the issue now is that the coordination is poor. Attempts are being done to balance wealth by assisting the lower income group but without clear strategies to promote investments, it is more of a rebalancing act to increase consumption growth. This can't last.

For Malaysia to grow, it will need private investments. Government sectors should be more of an enabler rather than competitor. This is where we have failed to address. While foreign investors are good for the country, in the longer run, local investors need to be competitive. There should also be a balance here as we tend to be overly dependent and eager to support foreign investors rather than local companies.

Our focus will have to change and I see there is a need for even Bursa to play its role.

Why is the government doing this? Before we go deep into the sectors and where should the growth be in Malaysia, let's look at the components of growth in the perspective of Malaysia and where should our focus be.

Let me put the context of economic growth to a simple 4 portions

GDP =

Consumption (C) + Investments (I) + Government Expenditures + Investments (G) + (Export(X) - Import (M))

Consumption (C) + Investments (I) + Government Expenditures + Investments (G) + (Export(X) - Import (M))

Consumption basically depends on the economic strength of the country and also how fast the velocity of the money flows. As a country we have been increasing and to a certain extent dependence on local Consumption for much part of our growth in the last 15 years. One can see through the strength of private consumption, so much so that our private debt to GDP exceeded 80% for quite a number of years now.

Investment (I) refers to in this case corporate private investor invests into the country. They may be foreign or local investor. One trend that we see nowadays is the public-private investment (PPI) initiatives as government will not be able to afford to invest and manage those projects themselves alone. Through an agency such as MIDA, we have also been encouraging foreign investments besides local.

Government (G) is where we see the expenditure of the government both in operational and capital expenditure. Both operational and capital are important as operational is where government employees' remunerations are paid as a consumer as well while developmental expenditure and mainly the investments which are made by government rather than private sectors. Examples of developmental expenditure are building of schools, hospitals, roads.

Lastly, the component of Exports (X) and Imports (M) which is highly relevant for a trading country like Malaysia. For certain industry, Import and Export goes hand in hand. Example trading industry. If there are no value add, then we are merely acting as traders. We import and export the same product. When there are value add for example, buying semiconductor components, materials - enhance them - we export them back into finished goods or more developed components. A strong country will be able to sell services as exports for example Intellectual Properties.

From the above, countries will work on various components in coordination among various departments, ministries. At different stages each country would develop their different components on various speed and level. Example, in the 1950s, US was pretty strong as an export country. Today, it is very a country doing much more Imports. China was such during its developmental years from 1980s until now. Recently, the internal policies have also been developing local consumption.

How do those four segments above interlinked. They are Vastly and Highly interlinked. Without investments for example, be it local or foreign, the Exports component will not be strong eventually. Without investments in ports, roads for example, there would not be further investments in trading, transportation, factories, housing.

Without strength in investments and Exports and Imports, we would not be able to grow our consumption. Malaysia was developing our local consumption sector post financial crisis in 1998/99. The velocity of the consumption will also create more consumption. However, for a country which is limited by its per capita income at a developing nation level, to grow consumption without focus on other components, higher debt will kick in. Too much debt is a problem as we have seen the collapse of the sub-prime housing crisis in US.

Malaysia is now at a stage where consumption is at its high while local private investments (non-GLCs) is tapering for some time now. We need to readjust. There is a need for more local private and foreign investments to promote strength in other segments.

I see that the government is aware of the above sporadically but the issue now is that the coordination is poor. Attempts are being done to balance wealth by assisting the lower income group but without clear strategies to promote investments, it is more of a rebalancing act to increase consumption growth. This can't last.

For Malaysia to grow, it will need private investments. Government sectors should be more of an enabler rather than competitor. This is where we have failed to address. While foreign investors are good for the country, in the longer run, local investors need to be competitive. There should also be a balance here as we tend to be overly dependent and eager to support foreign investors rather than local companies.

Our focus will have to change and I see there is a need for even Bursa to play its role.

Friday, November 22, 2019

Ekovest's acquisition of land from IWH: My take

What the deal is about.

Ekovest buying 2 blocks of land from IWH which IWH does not

own until this deal is done, ironically. Hence, IWH is actually acting as a middleman and

in return IWH owns 32% of Ekovest. Lim Kang Hoo will increase his shareholding

in Ekovest, backdoor through IWH as he is a larger shareholder of IWH through

Credence at 63.13%. Ekovest pays about RM200 million for the land and another

RM800 million through issuance of new ICPS (Irredeemable Convertible Preference

Shares) to IWH. The ICPS which is convertible to Ekovest’s shares at RM1 will

allow IWH to be a 32% shareholder of Ekovest. This will solidify LKH’s ownership of Ekovest.

His shareholding (direct and indirect) will increase from 29.8% to 44.4%.

The land was part of the land in the original exercise which

failed, in the proposed IWH-IWCITY merger back in 2017. As below, in that proposed deal, the merged entity is to acquire land from the same companies although not from as many sellers.

The deal has nothing to do with Bandar Malaysia, if any yet.

We know that IWH together with CREC was awarded with the contract for Bandar

Malaysia but details of the project is yet to be announced. The thing I can see

is that IWH is now getting closer to Ekovest. Whether it is good or bad, we do

not know. I can see that neither IWCITY or IWH are construction companies.

Ekovest is. Bandar Malaysia needs lot of these kind of work as the entire

development is RM140 billion in GDV. One will need a master developer and

master contractor. LKH is not going to let CREC take all.

For Ekovest’s shareholders, the situation is hard to read as we do not know

several things:

- We

do not know much about the deal between IWH and Straits Bay Sdn Bhd and Empomas

Holdings Sdn Bhd. Who are the owners? How are the payment made?

- Does

IWH has to pay cash to these guys? Or will IWH pay them in shares or any

other ways?

- Why

is IWH acquiring these 2 pieces of land? This looks questionable. Land in Johor will not see much development unless they are strategic to any government's projects in the near future. This I am not able to decipher.

One thing that is happening is that the owners of Ekovest are

thinking big. It is growing Ekovest in terms of market value at the expense of

dilution to minority shareholders. However, for the shareholders which include me, we know that the group is not staying put at 2 highways and a few plots of good land. The elephant in the room as all have been talking about is the old military airport land and its development.

I believe this is not the last of the deals.

Wednesday, November 20, 2019

WCE 2Q19: Commentaries on progress and accounting

WCE has just announced its financial report for 2Q19 which we would have expected as the company has yet to start toll operation. It has just reported a loss for the quarter and that is because it has to account for interest expense for the sections that is completed because it cannot capitalised the interest anymore. (These are accounting treatment but I do not see it starting to pay interest yet)

The higher finance costs can be seen as above. Its explanation is as per below.

Another point of note which we do not see in the previous announcements. This is more important as it foresees it will not be able to register profits for several years in its account as mentioned below due to interest expense which of course would be higher as it is bearing the full loan's interest in the early years as well as usual amortisation costs while waiting for the toll revenue to improve over time. However, we could see that the project to be cashflow positive as mentioned below. (I have mentioned before of losses in the early years while cashflow would be different) Of course these are all projections and forward looking statement.

It also mentioned that it expects to commence toll collection by December 2019. Let's see.

The higher finance costs can be seen as above. Its explanation is as per below.

Another point of note which we do not see in the previous announcements. This is more important as it foresees it will not be able to register profits for several years in its account as mentioned below due to interest expense which of course would be higher as it is bearing the full loan's interest in the early years as well as usual amortisation costs while waiting for the toll revenue to improve over time. However, we could see that the project to be cashflow positive as mentioned below. (I have mentioned before of losses in the early years while cashflow would be different) Of course these are all projections and forward looking statement.

It also mentioned that it expects to commence toll collection by December 2019. Let's see.

Sunday, November 17, 2019

Where are our stocks heading? Is Malaysia Inc. happening and strategies for our Bursa market. Part 1

At the time of writing, we already know of the landslide victory that BN had with its MCA's candidate winning more than 15,000 votes turning around a lost to a win. This by-election win by BN will bring a more challenging situation for the market at least for the next 1 year - if not beyond the GE 15.

This first part of the writing, I am focusing on Malaysia Inc. - a strategy that was close to Tun Mahathir during his 22 years tenure between 1980 till 2003. During then, we know that many government corporations were turned into corporate companies - from LLN to Tenaga Nasional, STMB to Telekom Malaysia Bhd and beyond which includes Axiata today. Bank Bumiputera through several exercises is a corporate that is now called CIMB.

We also have know of Tun Daim - the mastermind of Mahathir's Malaysia Inc. strategy with several associates which includes Halim Saad (UEM, Renong), Wan Azmi of Land and General, Tajuddin Ramli (the original Celcom owner and later MAS), Samsuddin from Granite Industries and several more. There were of course many businessmen whom have made it through that tenure of Tun Mahathir, as he is a person who is keen to allow capitalism to succeed. Those businessmen are Ananda Krishnan, Tan Sri Gnanalingam, YTL (of course), and to a lesser extent Genting's Lim Goh Tong and his son, Hong Leong's Quek Leng Chan and Tan Sri Mokhtar al-Bukhari.

After 9 May 2018, we would have expected the similar strategy to be revived. Khazanah Nasional among its first move was to sell off a stake in IHH - almost controlling stake - to Mitsui. There were talks of MAS being divested or investors invited, PLUS's stake being reduced or fully sold. Tun M himself had mentioned before he is more keen of government encouraging businesses to excel while the role of the government is to get a share of the profits through taxation.

Well, that strategy has yet to see any movement - at all - except for the IHH's stake sale. Even then, it was a change of shareholdings rather than management. As mentioned above, the Tanjung Piai's results may probably see the strategy which already as it is difficult - to be even more challenging. Mahathir will have groups whom will be objecting to several of his strategies, and he is running out of time. At the moment, nothing concrete is coming and we know that for any corporate moves to make them happen, will take a few years. Tun M does not have that time - more so there are 3 main parties involved (Bersatu, DAP and PKR - the other 2 Amanah and Warisan seems to have lesser say and would probably be more obliging). For any private companies, there is this worry as well additionally, will the next administration be open to private businesses.

After the 1998 Asian crisis, Khazanah if one can remember was growing and active. Several of its moves were to rescue companies like Time, UEM, Renong and Bank Bumiputera. If Tun M had his way, I believe that rescue were not meant to be for long. However, since then, administration changed twice and government linked companies were getting stronger. There are arguments that with government in business, it is curtailing the growth of private businesses. At the moment, about 15 companies under the KLCI are government controlled. Malaysia especially the GLCs head are already comfortable with GLCs controlled companies.

That situation is going to be hard to change. In the past, we parachuted business owners to own the business - think Tajuddin Ramli with MAS. I believe that will be very hard to happen given the challenge that Mahathir has - case in point PLUS. Khazanah is against it, the Finance Ministry is against it as well. One cannot fault these two entities to be against the purchases though, as PLUS is among the more lucrative assets that the government owns.

This is the reason why KLCI will be a bad performer

With about half of the companies under the KLCI government controlled and the strategies of the government in limbo, many investors rightfully would be staying on the sideline. It does not help when these counters are not cheap in their valuations. The ones that seem to do the supporting are again the government controlled funds. How much can they support as ultimately the one that is important is the financial results? That is also why GLCs cannot afford to slack. If any one of the company is slacking, it may impact KLCI. Example: Telekom Malaysia when a year ago the Minister in charge opened up the fiber broadband to other players. It was the right thing to do, but it affects Telekom and ultimately KLCI.

What do we do then?

We have to basically avoid the large counters especially the ones which are not founder or privately driven. When there are situations whether things will be changing or not is causing the GLC companies to be less attractive. When government is not coming up with a certain and solid direction, employees would be waiting at the side - doing the waiting game. That is not efficient.

If we want to still invest into Bursa, the way forward for now is to look for companies that are less impacted by government policies. And that is the one which I am going to discuss in my future article as Malaysia Inc. policies is not clear and it is not going to help either party.

This first part of the writing, I am focusing on Malaysia Inc. - a strategy that was close to Tun Mahathir during his 22 years tenure between 1980 till 2003. During then, we know that many government corporations were turned into corporate companies - from LLN to Tenaga Nasional, STMB to Telekom Malaysia Bhd and beyond which includes Axiata today. Bank Bumiputera through several exercises is a corporate that is now called CIMB.

We also have know of Tun Daim - the mastermind of Mahathir's Malaysia Inc. strategy with several associates which includes Halim Saad (UEM, Renong), Wan Azmi of Land and General, Tajuddin Ramli (the original Celcom owner and later MAS), Samsuddin from Granite Industries and several more. There were of course many businessmen whom have made it through that tenure of Tun Mahathir, as he is a person who is keen to allow capitalism to succeed. Those businessmen are Ananda Krishnan, Tan Sri Gnanalingam, YTL (of course), and to a lesser extent Genting's Lim Goh Tong and his son, Hong Leong's Quek Leng Chan and Tan Sri Mokhtar al-Bukhari.

After 9 May 2018, we would have expected the similar strategy to be revived. Khazanah Nasional among its first move was to sell off a stake in IHH - almost controlling stake - to Mitsui. There were talks of MAS being divested or investors invited, PLUS's stake being reduced or fully sold. Tun M himself had mentioned before he is more keen of government encouraging businesses to excel while the role of the government is to get a share of the profits through taxation.

Well, that strategy has yet to see any movement - at all - except for the IHH's stake sale. Even then, it was a change of shareholdings rather than management. As mentioned above, the Tanjung Piai's results may probably see the strategy which already as it is difficult - to be even more challenging. Mahathir will have groups whom will be objecting to several of his strategies, and he is running out of time. At the moment, nothing concrete is coming and we know that for any corporate moves to make them happen, will take a few years. Tun M does not have that time - more so there are 3 main parties involved (Bersatu, DAP and PKR - the other 2 Amanah and Warisan seems to have lesser say and would probably be more obliging). For any private companies, there is this worry as well additionally, will the next administration be open to private businesses.

After the 1998 Asian crisis, Khazanah if one can remember was growing and active. Several of its moves were to rescue companies like Time, UEM, Renong and Bank Bumiputera. If Tun M had his way, I believe that rescue were not meant to be for long. However, since then, administration changed twice and government linked companies were getting stronger. There are arguments that with government in business, it is curtailing the growth of private businesses. At the moment, about 15 companies under the KLCI are government controlled. Malaysia especially the GLCs head are already comfortable with GLCs controlled companies.

That situation is going to be hard to change. In the past, we parachuted business owners to own the business - think Tajuddin Ramli with MAS. I believe that will be very hard to happen given the challenge that Mahathir has - case in point PLUS. Khazanah is against it, the Finance Ministry is against it as well. One cannot fault these two entities to be against the purchases though, as PLUS is among the more lucrative assets that the government owns.

This is the reason why KLCI will be a bad performer

With about half of the companies under the KLCI government controlled and the strategies of the government in limbo, many investors rightfully would be staying on the sideline. It does not help when these counters are not cheap in their valuations. The ones that seem to do the supporting are again the government controlled funds. How much can they support as ultimately the one that is important is the financial results? That is also why GLCs cannot afford to slack. If any one of the company is slacking, it may impact KLCI. Example: Telekom Malaysia when a year ago the Minister in charge opened up the fiber broadband to other players. It was the right thing to do, but it affects Telekom and ultimately KLCI.

What do we do then?

We have to basically avoid the large counters especially the ones which are not founder or privately driven. When there are situations whether things will be changing or not is causing the GLC companies to be less attractive. When government is not coming up with a certain and solid direction, employees would be waiting at the side - doing the waiting game. That is not efficient.

If we want to still invest into Bursa, the way forward for now is to look for companies that are less impacted by government policies. And that is the one which I am going to discuss in my future article as Malaysia Inc. policies is not clear and it is not going to help either party.

Saturday, November 16, 2019

Positive trend from trade war should be coming through PIE Industrial and VS Industry

The early impact of trade war can be seen now. While companies are scrambling to reorganize their supply chain, within the short run we see deterioration of international trade. Yesterday, Malaysia announced a 4.4% GDP growth - not bad given the circumstances. Export sector has seen a drop expectedly. As discussed in my previous article, we will see some companies benefiting from the trade war while others may suffer. I foresee those that are benefiting in the long run would be

The announcement provided by Statistics Department which is not a surprise,

Malaysia’s exports of goods in the third quarter of 2019 recorded a decrease of 1.9 per cent to RM247.0 billion as compared to RM251.8 billion registered in the same period last year. The main products which attributed to the decrease were electrical & electronic products and crude petroleum that shrank by 4.9 per cent and 43.9 per cent respectively.

For PIE, it announced a better 3rd quarter results yesterday against previous quarter of 2Q19 as well as last year's quarter of 3Q18. While its profitability improved (due to foreign exchange gain, lower administrative costs, reversal of impaired collection), its revenue dropped a little.

It is a decent result given the circumstances. It is expected as US imposed additional tariff starting on 1 September 2019 causing companies to scramble to readjust. We seen the results impacting some companies but still VS and PIE are not affected as much. In the long run they will gain.

What is more important as has been provided by PIE is a guidance on what it expects for 2019 and beyond as below. From what we read, PIE may not increase its revenue substantially, but potentially the profit margin will increase. It is more selective in its business orders - something which one can do when times are better. It is better times potentially for Malaysian EMS companies. We see the same through VS Industry.

Current Year Prospect - PIE Industrial (3Q19)

The major source of revenue and profit of the Group is from its manufacturing segment (99%). For EMS activities (80%), orders are expected to increase in the long run from existing customers and potential new customers through its fully built-up vertical integrated manufacturing facilities which have been improved in operation for the past 5 years. Due to the beneficial effect of USA-China trade war, this division is expected to receive more orders from new overseas customers in 2019. This division will cancel certain new low-margin, high-volume products since beginning of 2019 and focus on profitable projects from potential new customers. The serious shortage of certain electronics component in 2018 is expected to be smoothen in coming quarters. However, any drastic fluctuation of Ringgit Malaysia against USD will be the main factor affecting its performance in the near future.

I see better performances for these companies in the EMS sector throughout next few years as the global trend is changing and for the better.

- PIE Industrial

- VS Industry

- Globetronics

- Pentamaster has shown a surprisingly positive results

While those whom will be immediately impacted are:

- Inari Amertron

- KESM

- Unisem

- Carsem (MPI)

- Aemulus

The announcement provided by Statistics Department which is not a surprise,

Malaysia’s exports of goods in the third quarter of 2019 recorded a decrease of 1.9 per cent to RM247.0 billion as compared to RM251.8 billion registered in the same period last year. The main products which attributed to the decrease were electrical & electronic products and crude petroleum that shrank by 4.9 per cent and 43.9 per cent respectively.

For PIE, it announced a better 3rd quarter results yesterday against previous quarter of 2Q19 as well as last year's quarter of 3Q18. While its profitability improved (due to foreign exchange gain, lower administrative costs, reversal of impaired collection), its revenue dropped a little.

It is a decent result given the circumstances. It is expected as US imposed additional tariff starting on 1 September 2019 causing companies to scramble to readjust. We seen the results impacting some companies but still VS and PIE are not affected as much. In the long run they will gain.

What is more important as has been provided by PIE is a guidance on what it expects for 2019 and beyond as below. From what we read, PIE may not increase its revenue substantially, but potentially the profit margin will increase. It is more selective in its business orders - something which one can do when times are better. It is better times potentially for Malaysian EMS companies. We see the same through VS Industry.

Current Year Prospect - PIE Industrial (3Q19)

The major source of revenue and profit of the Group is from its manufacturing segment (99%). For EMS activities (80%), orders are expected to increase in the long run from existing customers and potential new customers through its fully built-up vertical integrated manufacturing facilities which have been improved in operation for the past 5 years. Due to the beneficial effect of USA-China trade war, this division is expected to receive more orders from new overseas customers in 2019. This division will cancel certain new low-margin, high-volume products since beginning of 2019 and focus on profitable projects from potential new customers. The serious shortage of certain electronics component in 2018 is expected to be smoothen in coming quarters. However, any drastic fluctuation of Ringgit Malaysia against USD will be the main factor affecting its performance in the near future.

I see better performances for these companies in the EMS sector throughout next few years as the global trend is changing and for the better.

Friday, November 15, 2019

Interestingly Ekovest's venture into Musang King may have its leads

It started when Ekovest bought into PLS Plantation, acquiring a 23.42% from its Chairman, Lim Kang Hoo. This was a related party transaction and it looked particularly bad when it was the company one controls buying the shares from himself.

Secondly, it looked like a rescue of PLS Plantation. Immediately, after the purchase from LKH, Ekovest continuously bought more PLS shares from the market. Now, Ekovest owns 30.44% of PLS Plantation. First of all, PLS did not seem to be an interesting stock. One would wonder, why would a company that has good business concessions in Setiawangsa Pantai Expressway, DUKE and traditionally a decent construction outfit be keen in diluting itself into plantation. It is neither a strong palm oil stock nor any other plantation business for that matter. At around the same time, PLS announced that it was moving into durian plantation. It acquired a company called Dulai Fruits.

Wow! How is one to value a durian plantation business? Palm oil is difficult enough for a small to medium sized company. PLS was not profitable for last few years. Then durian? Worse, durian is seasonal. The only thing I can think of is the company's strong affiliation with China given it has business dealings with large companies there through Bandar Malaysia and Lim Kang Hoo's partnership with large developers from China through IWCity. China's Chinese adore durians - at the moment. The thing I learned about when I was in China recently - the typical supermart in China would sell durians - Thai's durian. We do not even see durians so commonly available in Malaysia. Also, Malaysia was only allowed to export whole durian fruit only recently. How then Chinese were able to taste Malaysian Musang King previously. I learned about this from a Singaporean in China. We used to export our Musang King via Thailand. That was how bad the situation.

Just recently, Navis Capital invested RM400 million into a Malaysian durian exporter, Hernan Corp. Navis being a long established private equity firm must have done research about durians. They must have seen a trend and China's appreciation of Malaysian durians. And this trend is not a passing trend - as like the bird's nest and arowana. China to me has changing habits. It seems that their reverence over durian may last longer, hopefully forever.

BFM's had an interview with the CEO of Hernan Corp. It is good knowledge for me, not just on perspective of durian business but also perhaps why Ekovest is into the business of Musang King. Perhaps, Lim Kang Hoo by going himself, he is not able to leverage on the durian trend on the large scale basis, and it needs to be done quick, as well.

For durian planters, it takes 5 years for any to start yielding results. That is the bad part. Bursa's investors do not like to wait for 5 or more years - I learned that from WCE. The good part is durian plantation is not an open competition situation. I believe that only a few countries can have that position given the costs of land, position, climate and costs. It can be a moat if done right as competition can be curtailed.

Now, it may not look that bad. Especially given that Bandar Malaysia is alive and back - the construction division will have continuous deal way past SPE while the plantation and toll concessions will bring the long term consistent revenue - ideally.

Secondly, it looked like a rescue of PLS Plantation. Immediately, after the purchase from LKH, Ekovest continuously bought more PLS shares from the market. Now, Ekovest owns 30.44% of PLS Plantation. First of all, PLS did not seem to be an interesting stock. One would wonder, why would a company that has good business concessions in Setiawangsa Pantai Expressway, DUKE and traditionally a decent construction outfit be keen in diluting itself into plantation. It is neither a strong palm oil stock nor any other plantation business for that matter. At around the same time, PLS announced that it was moving into durian plantation. It acquired a company called Dulai Fruits.

Wow! How is one to value a durian plantation business? Palm oil is difficult enough for a small to medium sized company. PLS was not profitable for last few years. Then durian? Worse, durian is seasonal. The only thing I can think of is the company's strong affiliation with China given it has business dealings with large companies there through Bandar Malaysia and Lim Kang Hoo's partnership with large developers from China through IWCity. China's Chinese adore durians - at the moment. The thing I learned about when I was in China recently - the typical supermart in China would sell durians - Thai's durian. We do not even see durians so commonly available in Malaysia. Also, Malaysia was only allowed to export whole durian fruit only recently. How then Chinese were able to taste Malaysian Musang King previously. I learned about this from a Singaporean in China. We used to export our Musang King via Thailand. That was how bad the situation.

Just recently, Navis Capital invested RM400 million into a Malaysian durian exporter, Hernan Corp. Navis being a long established private equity firm must have done research about durians. They must have seen a trend and China's appreciation of Malaysian durians. And this trend is not a passing trend - as like the bird's nest and arowana. China to me has changing habits. It seems that their reverence over durian may last longer, hopefully forever.

BFM's had an interview with the CEO of Hernan Corp. It is good knowledge for me, not just on perspective of durian business but also perhaps why Ekovest is into the business of Musang King. Perhaps, Lim Kang Hoo by going himself, he is not able to leverage on the durian trend on the large scale basis, and it needs to be done quick, as well.

For durian planters, it takes 5 years for any to start yielding results. That is the bad part. Bursa's investors do not like to wait for 5 or more years - I learned that from WCE. The good part is durian plantation is not an open competition situation. I believe that only a few countries can have that position given the costs of land, position, climate and costs. It can be a moat if done right as competition can be curtailed.

Now, it may not look that bad. Especially given that Bandar Malaysia is alive and back - the construction division will have continuous deal way past SPE while the plantation and toll concessions will bring the long term consistent revenue - ideally.

Wednesday, November 13, 2019

FAA's downgrade of Malaysian aviation - Impact to Malaysia's aviation

By now we would have read that the FAA downgrade of Malaysia's aviation safety rating has nothing to do with the airlines, but rather on the regulatory functions. This has caused concerns over some of us, when does not know how it is going to impact our aviation sector. One director went further by saying that the FAA would not have done check on us until Airasia X had its flight to Honolulu. In fact, since 2003, the FAA had not had a check on us. Is it a blame on Airasia X, or he is just saying a fact.

That same person runs Time Dotcom. I think he may have said a factual matter, but does it matter? Should it be because of a flight route initiated to Honolulu, we should now be putting our house in order - safety that it?

As a customer to airlines and the aviation industry, we have been bombarded by continuous price increases over the last few years. We created MAVCOM in 2015 which some say overlaps the function of CAAM. We even pay RM1 to support MAVCOM each time we take a commercial flight. I am sure given the continuous increase in passenger traffic, they should be sufficiently covered financially. It is ironic, that the users are the one that usually covers the expenses of these guys whereas their functions should be improving the infrastructure and profile of Malaysia as an aviation and tourism hub. The winner has been MAVCOM and the country but the users are the one who pay.

When we have CAAM whose salary scale follows the government and it is supposedly insufficient to entice the experienced people to stay, we have MAVCOM as well, whose role is still unclear.

How does this impact Malaysia? We have built a solid industry. I think it is time to be more vigilant and have the input from the right group of people for our aviation to grow.

That same person runs Time Dotcom. I think he may have said a factual matter, but does it matter? Should it be because of a flight route initiated to Honolulu, we should now be putting our house in order - safety that it?

As a customer to airlines and the aviation industry, we have been bombarded by continuous price increases over the last few years. We created MAVCOM in 2015 which some say overlaps the function of CAAM. We even pay RM1 to support MAVCOM each time we take a commercial flight. I am sure given the continuous increase in passenger traffic, they should be sufficiently covered financially. It is ironic, that the users are the one that usually covers the expenses of these guys whereas their functions should be improving the infrastructure and profile of Malaysia as an aviation and tourism hub. The winner has been MAVCOM and the country but the users are the one who pay.

When we have CAAM whose salary scale follows the government and it is supposedly insufficient to entice the experienced people to stay, we have MAVCOM as well, whose role is still unclear.

How does this impact Malaysia? We have built a solid industry. I think it is time to be more vigilant and have the input from the right group of people for our aviation to grow.

Saturday, November 9, 2019

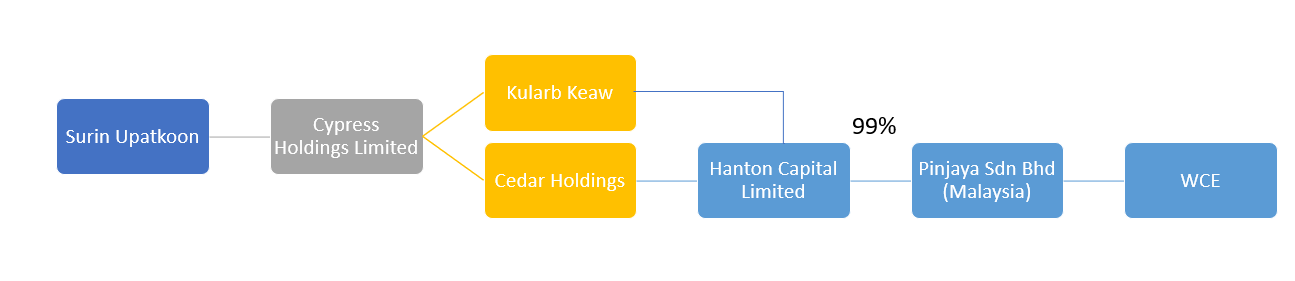

Surin Upatkoon's new holding structure in WCE: Cleaner, better

I have been asked on the new structure for the second largest shareholder of WCE: Surin Upatkoon. What are the impact? Is he relinquishing his stake in WCE etc.?

Well, as a start his original stake in WCE is through several organizations i.e. a complex holding via 5 companies namely, Cypress Holdings Limited, Pinjaya Sdn Bhd (Malaysia), Hanton Capital Limited, Cedar Holdings Limited, Kularb Kaew Company Limited

The shareholding was as depicted below:

With the exercise, it seems that the shareholding is now cleaner i.e. as below:

As in the announcement, Hanton Capital, a company resided in a tax haven, Virgin Islands has sold its 99.9% stake of Pinjaya directly to Tan Sri Surin Upatkoon.

Well, I prefer this as it is cleaner and the actual shareholder is now back into Malaysia.

What makes it change then, as sometimes business people would prefer a more complex structure.

That could be due to several reasons:

Well, as a start his original stake in WCE is through several organizations i.e. a complex holding via 5 companies namely, Cypress Holdings Limited, Pinjaya Sdn Bhd (Malaysia), Hanton Capital Limited, Cedar Holdings Limited, Kularb Kaew Company Limited

The shareholding was as depicted below:

With the exercise, it seems that the shareholding is now cleaner i.e. as below:

As in the announcement, Hanton Capital, a company resided in a tax haven, Virgin Islands has sold its 99.9% stake of Pinjaya directly to Tan Sri Surin Upatkoon.

Well, I prefer this as it is cleaner and the actual shareholder is now back into Malaysia.

What makes it change then, as sometimes business people would prefer a more complex structure.

That could be due to several reasons:

- He just want a cleaner structure (surprisingly)

- Because of the rights issue, he may use bank financing to fund part of his subscription. Banks usually prefer a cleaner structure especially when they are the one financing the purchase.

- If one is to notice above, the holding is brought back to Malaysia. As toll business has gone riskier due to the threat of government's plan of toll elimination, I believe foreign financiers are more reluctant to finance it. The financing may be dependent on local banks and they do not want to be seen financing a company with complex web of structure.

If Surin relinquishing his holdings in WCE? I think not at all, especially when he privatised MWE partly because of this.

Is there an impact on WCE? Minimal. But I prefer this structure better.

Free warrants and its futility

Free warrant feels like this. If we give it the first time, the children (meaning the ones that are still immature) will like it - feels like free ang pows. Precisely. But soon, the children will also realise that the free ang pows that we give is just a paper money which is worth less when we print our own money.

If we give out too many times just like what Vivocom did - in total 5 times and see what happened to its share price. Vivocom used to be the master of the free warrants and seems like one person - a sifu - is a biggest proponent of free warrants.

I wrote an article about Vivocom, during its most active period.

What is free warrant?

It is printing money. Only one country in this world can do it in large quantities and can get away with it. Uncle Sam. Even then, they are rethinking.

One person used to say this,

You can fool all the people some of the time, and some of the people all the time, but you cannot fool all the people all the time.

But it seems that recently, Buffettology is also under fire by some people. Nothing wrong and harmful.

If we give out too many times just like what Vivocom did - in total 5 times and see what happened to its share price. Vivocom used to be the master of the free warrants and seems like one person - a sifu - is a biggest proponent of free warrants.

I wrote an article about Vivocom, during its most active period.

What is free warrant?

It is printing money. Only one country in this world can do it in large quantities and can get away with it. Uncle Sam. Even then, they are rethinking.

One person used to say this,

You can fool all the people some of the time, and some of the people all the time, but you cannot fool all the people all the time.

But it seems that recently, Buffettology is also under fire by some people. Nothing wrong and harmful.

PLUS's press statement shows they are out of touch with their customers

PLUS largely operates along the North-South Highway and also the urban areas where its highway passes through Damansara right down to Klang (NKVE) while its Elite Highway passes through part of Shah Alam and connects to KLIA/KLIA2 from Damansara. PLUS obviously has the best highway in the country besides LDP in the urban areas.

Recently, it came out with a practice by not allowing motorists to do their top-up through its booths but instead pushing the motorists to top up counters at various counters at the side of the highways. I am not against the move as it does smoothen the traffic as queues do create unnecessary traffic along the toll booths. However on the other hand, practices like this creates complains from the toll users as some of them could not use the convenience of the booths for top ups, whereas they have to stop at stops to do the top ups.

The CEO of PLUS, came out and defended the company's move as it claims that motorists, due to this practice, top-up a higher amount each time whenever on average. It sounds as the right thing to do. However, if we try to understand the reason for some of them to do micro top-ups of RM10 and RM20, we can see and understand the financial situation of these people. A lot of these guys are also Grab or e-hailing drivers. In a few instances, the Grab drivers even asked me for cash to top up their pre-paid cards.

I think in many cases nobody wants to do micro top-ups if they can afford to but they just do not want their money to be tied down to the cards. That's what it is, in general.

Hope that a large company like PLUS can be more empathetic.

Recently, it came out with a practice by not allowing motorists to do their top-up through its booths but instead pushing the motorists to top up counters at various counters at the side of the highways. I am not against the move as it does smoothen the traffic as queues do create unnecessary traffic along the toll booths. However on the other hand, practices like this creates complains from the toll users as some of them could not use the convenience of the booths for top ups, whereas they have to stop at stops to do the top ups.

The CEO of PLUS, came out and defended the company's move as it claims that motorists, due to this practice, top-up a higher amount each time whenever on average. It sounds as the right thing to do. However, if we try to understand the reason for some of them to do micro top-ups of RM10 and RM20, we can see and understand the financial situation of these people. A lot of these guys are also Grab or e-hailing drivers. In a few instances, the Grab drivers even asked me for cash to top up their pre-paid cards.

I think in many cases nobody wants to do micro top-ups if they can afford to but they just do not want their money to be tied down to the cards. That's what it is, in general.

Hope that a large company like PLUS can be more empathetic.

Thursday, October 31, 2019

What Paul Krugman says about debt

Paul Krugman, the controversial Nobel Prize economist, who coincidentally penned an article about capital control and advice Asian countries on the matter one day before Malaysia had its capital control on 1 Sep 2018 - and the rest is history - politically and economically for Malaysia.

He has this to say about debt and its misconception (piece written on The New York Times) and I think this has its relevance to the Malaysian economy today although it was pointed towards the US.

----------------------------------------------------------------------------------------------------------------

People still don’t understand debt

By Paul Krugman

Opinion Columnist (29 Oct 2019)

Today’s column is about our trillion dollar deficit, which nobody seems to care about. The thing is, this lack of concern is justified: There’s no good reason to believe that the current budget deficit is doing significant harm.

What did do a lot of harm was the deficit hysteria that dominated establishment discourse the last time we had a deficit this big, which also happened to be a period during which the economy was deeply depressed, and the stimulus from deficit spending was actually a good thing. It should have been obvious that obsessing about deficits in 2012 was a huge mistake. What’s relatively new — and something I couldn’t get into at length in the column — is the realization that government debt isn’t much of a problem even at full employment.

One reason people find this hard to understand is that they make an analogy between the nation as a whole and an individual family. This leads to sober-sounding warnings that budget deficits amount to stealing from our children, in the same way that spendthrift parents are squandering their heirs’ inheritance.

This analogy, however, is all wrong. Debt is money we owe to ourselves — that is, for the most part it obliges one group of Americans, taxpayers, to make payments to another group of Americans, bondholders. It doesn’t directly make the nation poorer, at all. (O.K., there’s a small caveat: some debt is held by foreigners. But it’s not quantitatively important.)

Now, there might be indirect ways in which debt makes us poorer. To pay interest, the government might have to spend less or collect more taxes than it would have otherwise. And this could hurt growth — for example, high taxes could reduce incentives to produce and invest.

What economists have come to realize, however, is that even these indirect costs of debt may be negligible.

Why, after all, must a government raise taxes to deal with a higher level of debt? The usual answer is that if it doesn’t, the debt will snowball: the government will have to pay more in interest, which will cause the debt to rise further, leading to even more interest payments, and so on.

But nobody cares about the absolute value of debt; what matters is the ratio of debt to the tax base, which for the federal government is basically the whole economy, i.e., G.D.P. And a rise in the debt/G.D.P. ratio doesn’t snowball — it melts! Why? Because the interest rate on federal debt is normally lower than the economy’s growth rate.

He has this to say about debt and its misconception (piece written on The New York Times) and I think this has its relevance to the Malaysian economy today although it was pointed towards the US.

----------------------------------------------------------------------------------------------------------------

People still don’t understand debt

By Paul Krugman

Opinion Columnist (29 Oct 2019)

Today’s column is about our trillion dollar deficit, which nobody seems to care about. The thing is, this lack of concern is justified: There’s no good reason to believe that the current budget deficit is doing significant harm.

What did do a lot of harm was the deficit hysteria that dominated establishment discourse the last time we had a deficit this big, which also happened to be a period during which the economy was deeply depressed, and the stimulus from deficit spending was actually a good thing. It should have been obvious that obsessing about deficits in 2012 was a huge mistake. What’s relatively new — and something I couldn’t get into at length in the column — is the realization that government debt isn’t much of a problem even at full employment.

One reason people find this hard to understand is that they make an analogy between the nation as a whole and an individual family. This leads to sober-sounding warnings that budget deficits amount to stealing from our children, in the same way that spendthrift parents are squandering their heirs’ inheritance.

This analogy, however, is all wrong. Debt is money we owe to ourselves — that is, for the most part it obliges one group of Americans, taxpayers, to make payments to another group of Americans, bondholders. It doesn’t directly make the nation poorer, at all. (O.K., there’s a small caveat: some debt is held by foreigners. But it’s not quantitatively important.)

Now, there might be indirect ways in which debt makes us poorer. To pay interest, the government might have to spend less or collect more taxes than it would have otherwise. And this could hurt growth — for example, high taxes could reduce incentives to produce and invest.

What economists have come to realize, however, is that even these indirect costs of debt may be negligible.

Why, after all, must a government raise taxes to deal with a higher level of debt? The usual answer is that if it doesn’t, the debt will snowball: the government will have to pay more in interest, which will cause the debt to rise further, leading to even more interest payments, and so on.

But nobody cares about the absolute value of debt; what matters is the ratio of debt to the tax base, which for the federal government is basically the whole economy, i.e., G.D.P. And a rise in the debt/G.D.P. ratio doesn’t snowball — it melts! Why? Because the interest rate on federal debt is normally lower than the economy’s growth rate.

Sunday, October 27, 2019

I doubt trade war will end soon and what we should do about it

In a forum I attended, one senior director of a large semiconductor multinational based in Penang told us not to look too much into the situation. That was May, few months later Trump increased tariffs for the same Chinese products by another 5%. For people who have been thinking that Trump is the bad guy, perhaps we should rethink. All the presidential candidates that have been asked on this topic, either they have tried to avoid this question or they have answered that they would have addressed the trade friction differently. Basically, they would also put pressure onto China.

Historians called this as "Thucydides's Trap", where it basically occurs when one up and coming super power emerges, challenging the reigning power that be, then the theory is a war can't be avoided. Thankfully, for several times war had been avoided and these seems to be avoided more recently example when US's economy exceeded Great Britain in 1900th. Today, who would allow a disastrous nuclear war where it would have a lose-lose proposition for the world.

China's GDP is expected to surpass US in the next decade and to many, it is a matter of time, not whether it will happen. China is promoting hard on Made in China 2025 policies where the plan extends up to 2049 - the 100 year anniversary of the Chinese Communist Party's reign over China. That also seems to be the date where silently China is planning for its military strength to exceed US.

Let me ask this question. Who would have expected this situation to happen even say 10 years ago? With the situation, do we think US will sit still?

If it is not Trump, the next President of United States - whether by 2021 or 2025 - does that person want to be remembered as a president where his office be seen historically as the one succumbed to another new power. Is there also a reason why China has allowed Xi Jinping to remain as president beyond the traditional 10 years?

So, are we naive enough to think that US will let this one go past them although the trend seems to put them in the losing situation.

China knows this and they can be seen to try their level best to address this. At the back of their mind though, they are willing to suffer in the short term but allowing their position to be stronger in the long run. In business, the Chinese businessmen are much short term in their actions, but when comes to the government, the Chinese government is hugely long term in their planning. US is the one which is not able to plan and act long term - because their financial and political system do not allow them to do that. Trump is up for election soon and he has to have actions that is based on that 2020 election, i.e. creating positions for his voter base while President Xi can afford to sit and wait.

Well what do we as Malaysians can expect to see and take advantage of

Two words. Trade and Technology

If we are dependent on consumption to drive our economy, I think that has been the story for the past 18 years. Today, it is much harder to drive consumption when our private debt is at 80+%. What we can hope for is the growth to be consistent while allowing other components of the GDP (i.e. Investment and Trade {Export - Import}) to drive through our economy. The government sadly has been focusing on balance of wealth - not wrong - but to drive equal prosperity, one country has to be prosperous first. How to distribute wealth when we do not have them? If we are not careful, the word prosper would not even be there as global competition today is so extreme that many countries can surpass us especially through trade.

Now Trade. We have learned about the Malacca history. Malaysia is lucky to be geographically strategic. Remember, the early days who were the ones trading in Malacca? Indians and Chinese. We happen to have those culture and people who speak the languages, hence the Indian and Chinese culture are a benefit rather than the a con. The vernacular schooling system could turn out to be an advantage rather than seemed to be a disadvantage. The only thing which Malaysia can't seem to let go is the pride factor.

Anyway, our government - past and present, know trade is important but how they do the execution is all that matters. If in the past Vietnam was at war, today it is in the most active in its investment policies. The Indonesian president seems to be inviting people of the right background to helm its important trade posts, although how it executes is key. So are China and India themselves. The Malaysian position today is not the same as the Malaysian of 25 years ago when we were knocking onto the door among the "Tiger" economies.

To claim that we can go back to our good old days of being seen as a prospective "Tiger economy" is just a saying if we do not focus on TECHNOLOGY.

Today, what US is afraid of China is not so much of its economic strength. US is more wary of China's technology prowess. The growth of Huawei and China's high-speed train technology, for example awakens many countries globally. And that country is hungry. Very hungry, and for a huge country it seems to be able to work in tandem to achieve its goal.

While we see China having its enterprise Alibaba claiming and coming here to teach Malaysians how to do e-commerce, we as a country have stagnated in our technology prowess and that area of investments especially. Just 20 years ago, the China government was hugely grappling with a new technology and phenomenon called the "Internet" as it was afraid of its effect towards freedom of speech. Today, that country is thriving out from that while we are still wondering what happened to our Multimedia Super Corridor.

To move Malaysia in the right direction, we have to revisit back what we try to do with our technology companies. While we invite Gojek here, we have to invest into a Gojek competitor. We have to do much more than giving RM300,000 to a Cradle recipient company and leave them with just the money. The worse that a Malaysian company has done is when our companies - GLCs included - having and giving more trusts to another company from abroad rather than providing a platform for our local companies to succeed. Sometimes having meritocracy in our procurement may not be a good thing especially when we do not allow our own companies to try and fail.

Malaysia today, seems to be running out of idea to expand our economy on especially the capital market - so much so that we are planning to list Petronas Carigali. Well, to list an oil and gas exploration business, we are not looking forward. We do not have the next new story.

We have to give encouragements and opportunities to more Vitrox-es and Penta. We have to give more capital opportunities to technology companies. LEAP is not doing its job given the acronym as it is too restrictive when comes to trade for example. The middlemen at the end of the day are the ones that make money as raising RM3 million can costs RM1 million.

We really have to move fast as if we are not careful, Bursa may not even be relevant.

Historians called this as "Thucydides's Trap", where it basically occurs when one up and coming super power emerges, challenging the reigning power that be, then the theory is a war can't be avoided. Thankfully, for several times war had been avoided and these seems to be avoided more recently example when US's economy exceeded Great Britain in 1900th. Today, who would allow a disastrous nuclear war where it would have a lose-lose proposition for the world.

China's GDP is expected to surpass US in the next decade and to many, it is a matter of time, not whether it will happen. China is promoting hard on Made in China 2025 policies where the plan extends up to 2049 - the 100 year anniversary of the Chinese Communist Party's reign over China. That also seems to be the date where silently China is planning for its military strength to exceed US.

Let me ask this question. Who would have expected this situation to happen even say 10 years ago? With the situation, do we think US will sit still?

If it is not Trump, the next President of United States - whether by 2021 or 2025 - does that person want to be remembered as a president where his office be seen historically as the one succumbed to another new power. Is there also a reason why China has allowed Xi Jinping to remain as president beyond the traditional 10 years?

So, are we naive enough to think that US will let this one go past them although the trend seems to put them in the losing situation.

China knows this and they can be seen to try their level best to address this. At the back of their mind though, they are willing to suffer in the short term but allowing their position to be stronger in the long run. In business, the Chinese businessmen are much short term in their actions, but when comes to the government, the Chinese government is hugely long term in their planning. US is the one which is not able to plan and act long term - because their financial and political system do not allow them to do that. Trump is up for election soon and he has to have actions that is based on that 2020 election, i.e. creating positions for his voter base while President Xi can afford to sit and wait.

Well what do we as Malaysians can expect to see and take advantage of

Two words. Trade and Technology

If we are dependent on consumption to drive our economy, I think that has been the story for the past 18 years. Today, it is much harder to drive consumption when our private debt is at 80+%. What we can hope for is the growth to be consistent while allowing other components of the GDP (i.e. Investment and Trade {Export - Import}) to drive through our economy. The government sadly has been focusing on balance of wealth - not wrong - but to drive equal prosperity, one country has to be prosperous first. How to distribute wealth when we do not have them? If we are not careful, the word prosper would not even be there as global competition today is so extreme that many countries can surpass us especially through trade.

Now Trade. We have learned about the Malacca history. Malaysia is lucky to be geographically strategic. Remember, the early days who were the ones trading in Malacca? Indians and Chinese. We happen to have those culture and people who speak the languages, hence the Indian and Chinese culture are a benefit rather than the a con. The vernacular schooling system could turn out to be an advantage rather than seemed to be a disadvantage. The only thing which Malaysia can't seem to let go is the pride factor.

Anyway, our government - past and present, know trade is important but how they do the execution is all that matters. If in the past Vietnam was at war, today it is in the most active in its investment policies. The Indonesian president seems to be inviting people of the right background to helm its important trade posts, although how it executes is key. So are China and India themselves. The Malaysian position today is not the same as the Malaysian of 25 years ago when we were knocking onto the door among the "Tiger" economies.

To claim that we can go back to our good old days of being seen as a prospective "Tiger economy" is just a saying if we do not focus on TECHNOLOGY.

Today, what US is afraid of China is not so much of its economic strength. US is more wary of China's technology prowess. The growth of Huawei and China's high-speed train technology, for example awakens many countries globally. And that country is hungry. Very hungry, and for a huge country it seems to be able to work in tandem to achieve its goal.

While we see China having its enterprise Alibaba claiming and coming here to teach Malaysians how to do e-commerce, we as a country have stagnated in our technology prowess and that area of investments especially. Just 20 years ago, the China government was hugely grappling with a new technology and phenomenon called the "Internet" as it was afraid of its effect towards freedom of speech. Today, that country is thriving out from that while we are still wondering what happened to our Multimedia Super Corridor.

To move Malaysia in the right direction, we have to revisit back what we try to do with our technology companies. While we invite Gojek here, we have to invest into a Gojek competitor. We have to do much more than giving RM300,000 to a Cradle recipient company and leave them with just the money. The worse that a Malaysian company has done is when our companies - GLCs included - having and giving more trusts to another company from abroad rather than providing a platform for our local companies to succeed. Sometimes having meritocracy in our procurement may not be a good thing especially when we do not allow our own companies to try and fail.

Malaysia today, seems to be running out of idea to expand our economy on especially the capital market - so much so that we are planning to list Petronas Carigali. Well, to list an oil and gas exploration business, we are not looking forward. We do not have the next new story.

We have to give encouragements and opportunities to more Vitrox-es and Penta. We have to give more capital opportunities to technology companies. LEAP is not doing its job given the acronym as it is too restrictive when comes to trade for example. The middlemen at the end of the day are the ones that make money as raising RM3 million can costs RM1 million.

We really have to move fast as if we are not careful, Bursa may not even be relevant.

Saturday, October 26, 2019

Why the fundamentals for WCE does not change much

When I bought this share 6 years ago, I was looking really long term. Today, that mindset does not change. Sure enough, today the project faces some blip - not entirely due to the current government as they have promised the elimination of toll but also because there was a dispute over the alignment prior to that. Now, let us review what actually had happened and probably I will go through the bad news first.

Early delays

The alignment for Phase 7 had been changed as earlier the concessionaire faced a dispute from the government then on the alignment. Since then, it has been solved (after the change of government). This has caused delay in that phase and since it is a 50 + 10 year concession, the affect does not change much. Probably the biggest change was the cost of land acquisition has increased.

Threat over toll elimination by current government

I have written a piece on this after the change of government on May 9. So far, what is negative since then for WCE is that they have yet to collect toll despite completion certain sections. What was sort of promised by the government i.e. to eliminate tolls and force it onto the concessionaires i.e PLUS, Gamuda etc. did not happen. In fact, Gamuda's concessions is being bought at a fair price. In the event WCE is being forced to sell, they would be selling at a fair price as well.

Anyway, as we can see the government may not have the funds to purchase many of the concessions. Hence, it is possible the government is using Khazanah to purchase them. My question is this, if the idea of the current government is to privatise businesses, then this action acts on the opposite. Khazanah buying the concessions, would also mean they are collecting toll as well. Anyway, in the event Khazanah is buying, I think it is a a fair price of the concession, hence much higher value than what is being traded at - for WCE.

PLUS is being reviewed i.e. reduced toll rates

As in the Budget 2020, the government has promised that the toll rates for PLUS is reduced at least 18%. Well, it shows how profitable PLUS is. Despite not increasing the toll rates every 5 years, it can now afford to reduce the rates. Given the situation, I am not sure who will get (to purchase) the concessions, but surely we as EPF contributor is affected by the reduced rates collection.

The affect to WCE is probably minimal as I do not think over a long distance (from Shah Alam to Penang) driving the drivers would bother over few ringgit savings.

Increased value in land purchase

To me, this is the biggest negative, as it affects the pocket directly. Anyway, as mentioned in the prospectus, the land purchase deals 95% of them have been completed. What is done is done. WCE is disputing some of the acquisitions in court and it seems to be able to win a portion of it.

The increase in equity injection would affect the calculation of IRR in the project - assuming it is decently profitable around 10%. Any increase in equity would change the IRR and if we can remember the project has a IRR hurdle where in the event the concession's profits exceeds certain threshold, it is supposed to share a higher portion of the profits with government.

In the long run, hence the additional injection would not change much fundamentally given the IRR scenario.

Partial completion of the highway

This is the good part. It shows that the project is on the way and WCE is able to complete it. There is no reason to not believe they are capable of constructing despite the small situation over at Phase 4.

This project which has been talked about for so long is now really moving. The biggest beneficiary is Perak especially Lumut and I am sure many are waiting for the completion.

It is a long term project

Again, whatever the share price changed in the short term, there is little impact. At the moment, WCE has yet to collect toll so the financials that we see on quarterly and annually basis is no relevance. The biggest relevance is the costs and progress of construction.

Losses in the first few years

I have been asked on this, and would like to clarify. Profit and losses is not the main basis for calculation, as it is accounting (little bit deep to write in this article). What is important after the project is the cashflow. As an example, PLUS today on paper is making losses and I have read the Minister in past gladly presented the loss making fact (this loss actually is good for PLUS owners given the tax planning situation).

Let me put this in perspective, if it is making losses, why are there so many wanted to offer the purchase of PLUS?

Post 2038

There is potentially one big factor when PLUS is taken out of the tolls collection. Although PLUS is a parallel highway to WCE, there are various trends which is positive for WCE. One of them Pulau Indah port. WCE is closer to Pulau Indah, and the government is developing those areas. It is encouraging the expansion of the ports or even a new one. By then, given the development, WCE will have its own additional strength. As mentioned in past by the management, WCE's strength is its flat terrain which is a bonus for heavy vehicles.

I believe the traffic is so heavy by 2038 that, PLUS will be quite badly congested that we would have needed an alternative highway anyway. Hence WCE. I have also seen the maintenance of a non-tolled highway in Malaysia - which is not a good sight.

Early delays

The alignment for Phase 7 had been changed as earlier the concessionaire faced a dispute from the government then on the alignment. Since then, it has been solved (after the change of government). This has caused delay in that phase and since it is a 50 + 10 year concession, the affect does not change much. Probably the biggest change was the cost of land acquisition has increased.

Threat over toll elimination by current government