This is not a company one should bother looking at, however I am pulling out the Balance Sheet of the company to highlight how bad the asset portion can be for the company. Yes, assets can be bad as to liabilities can be good! It is not confusing while I will just highlight on a company with bad assets today and present another that has a presumingly good liabilities on another article.

EAH's Balance Sheet

Notice the remark side below. What consists of bad assets i.e. one which you do not want to have, as too much can be a bad thing. For EA below, you can assume that it reportedly has a Net Asset of RM55.5 million. Well, this is what it reports in its Annual Report but what it does not highlight in the chart section is that its intangible asset is RM24.7 million. Hence making its Net Tangible Asset at RM30.8 million. Not so great yeah since I have not heard of the company before and its intangible strength may not be of a Coca-cola or even Apple. How valuable are the intangibles really? If you look further, EA bought an IT company call DDSB Sdn Bhd in August 2010 for RM19.4 million and due to that purchase, close to RM18 million is consolidated as goodwill.

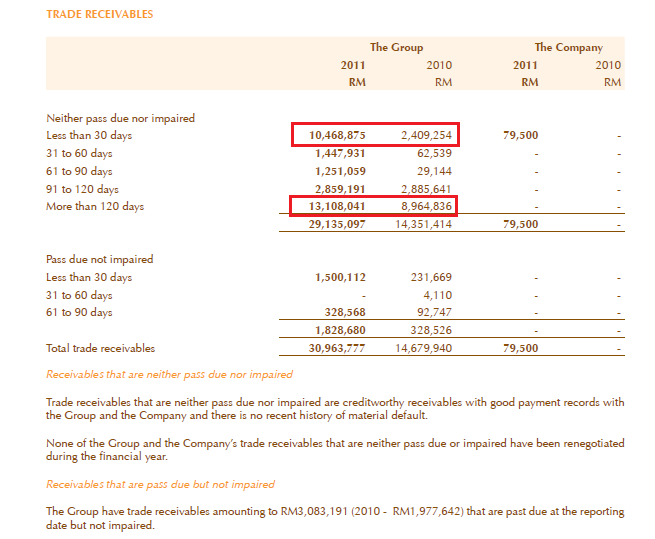

What other bad assets that the company has? In business, if the trade receivables

is manageable, it is manageable and we should be able to sleep knowing

that it is collectible within the credit timeframe. However, what

happens when your total receivables are close to your last year's total revenue? This is the case with EA Holdings.

Look further on the trade receivables - a bad asset

Let's look further on its trade receivables in details. RM13 million of collectibles which is more than 120 days? Well, you may say that out of the RM30 million, around RM10.5 million is in the less than 30 days column. However, I can also ask for the entire year's revenue of RM36.6 million for 2011, at least RM10.5 million is registered in the final month? Are we saying that the company is registering at least 30% of the total revenue in the final month? They can claim that since the company is a project based company, their revenue can be lumpy. You have to convince me more than that.

Now, you know why it can be regarded as a bad asset? In this case, receivables may not seem to be as liquid as it seems. Sometimes, one may look at just the total current asset but imagine what if a large portion of the receivables is being placed on the cash and cash equivalents row rather. The total current assets remain the same but the liquidity of the company is much stronger.

Profit and Loss Statement below to show that its revenue for the year was RM36.6 million, Although it can register a nice profit of RM11.8 million, with this kind of balance sheet, is it justified?

You know what if you look further to its balance sheet for 31 March 2012, it has gone further worse.