Most investors are wary of Chinese red chips stocks. It has happened in US, Singapore and more recently Malaysia. We just do not trust the accounts and we do not know how to address that. The most recent case is China Stationery where the company had one worrying sign after another:

- change of auditor - last year where Grant Thornton Foo Kon Tan resigned - one big warning sign;

- fire to one of its factories - when times are bad, a fire would partly solve it as it would have erase a lot of records, if needed to;

- resignation of directors - 1 just resigned a fortnight ago; and

- auditor's disclaimer.

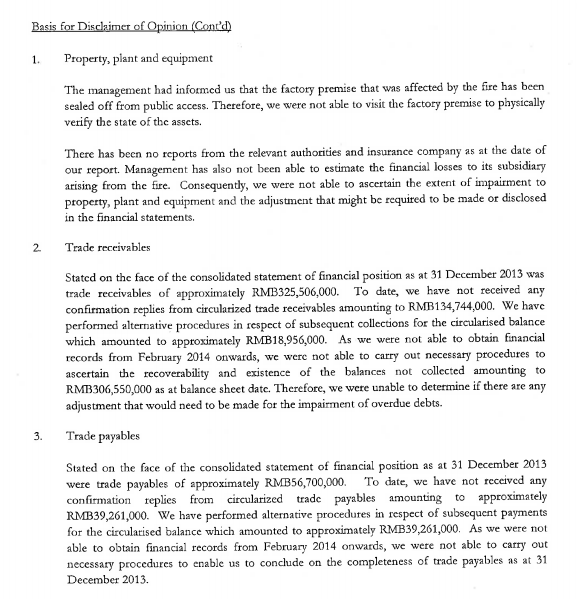

When an auditor disclaim its findings, we have to read what it disclaims - as below.

Ironically, it does not disclaim the cash position of the company, in which case it is very substantial. This also points to me that after having audited through the account, except for the items above that it disclaim or basically telling people it is unsure of, the cash position is verified. Below is part of its position of its balance sheet where it has RMB2.366 billion cash or RM1.2 billion. CSL's current traded value is RM124 million i.e. 10x below its cash holdings!

Did the fire burn any of those cash? Not possible as it would most definitely be in the bank.

Can we trust the bank statement? I don't know! As too many things have happened to the company until I do not know what to trust and that means, we have to take the accounts that the auditor signed-off as still questionable?

+announcement.png)