If we noticed the market nowadays, it has been much more on sentiments rather than being rational. There's a lot more trading activities today where even the large funds are taking part. The emergence of retail players a.k.a. the "Robin Hood"s investors is allowing much more purchases based on sentiments. There are possibly tonnes of Telegram and Youtube groups advising people where and how to invest. When I switched on youtube channels on investments, even Gurmit Singh (Phua Chu Kang) in partnership with a young investor advisor is involved.

With this I would deem that there's opportunities to search for value. The rubber gloves companies do not need any more introduction as there are just too much "noise" out there. On my part I see that although vaccine is on the way and few countries (Israel, UK, maybe US) have shown good progress from the vaccination program, I believe it will take years before COVID will be fully addressed. In the past I was just too optimistic. Even as at now, many countries are seeing fresh highs as people get more agitated due to the length of the pandemic and they just take less precautions.

Even most economies could not bear the brunt of inactivities and they just have to open up. One do not need to look far but at Malaysia. Many governments are taking the stand that they just need to allow economies to work for its money (with conditions).

The first round of MCO, there was money being ditched out to people (Makcik Kiah), Second round there were more funds but lesser amount. Moratorium for loans were introduced and practiced during the first six months. Those have stopped. Now, it is much more targeted assistance and even then they are in small bits and pieces.

I believe those similar situations are being practiced in many other countries which are developing when the virus is still rampant. In India, I was expecting the collapse of the health situation many month ago but it seems that they were contained - possibly because of people were willing to adhere to SOPs - and human beings especially from the democratic block were only willing to adhere to so as much. Now we see the brunt of what COVID can do to a country like India (with 1.3 billion people), poor developing country and with lack of basic discipline.

Hence, COVID is here to stay for a while even with vaccines.

For gloves, there is no doubt there will be more companies starting to produce more. But the demand will still be outstripping supply until to a point when COVID is addressed. Even then, let's think through - with a pandemic this scale, many countries would be looking at relooking at their capacity to address the next pandemic. I do not think gloves will be much oversupplied for a while because of this.

I know that certain countries would be looking at gloves self-sufficiencies at some of point of time but there are just few countries which are manufacturing scale developed - which is why Malaysia is one of the beneficiaries from the gloves manufacturing capabilities.

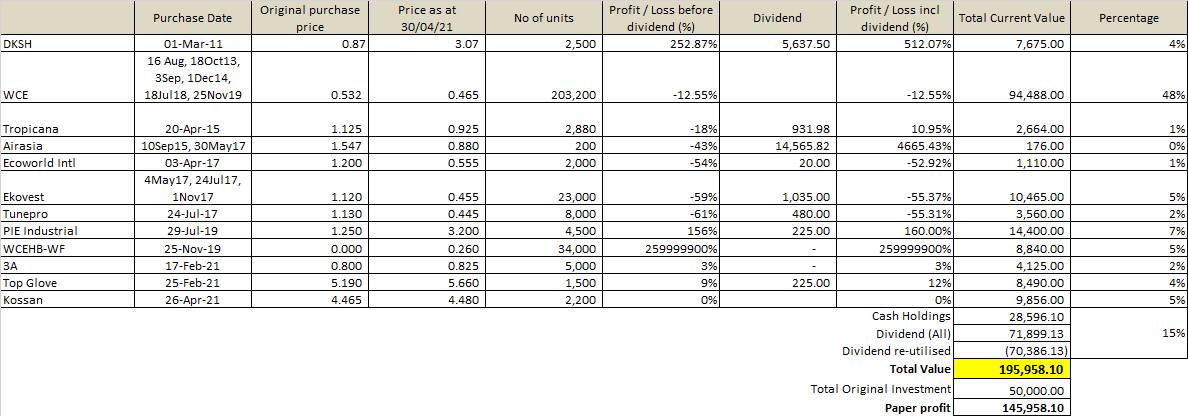

Due to the above, I have hence bought Kossan (2200 units) for the Felice's Fund.

From 2 months ago until now, I have also sold some 3A and redeemed TA due to its delisting.

As for the latest fund position, it is as below.