Sunday, August 21, 2022

Monday, May 3, 2021

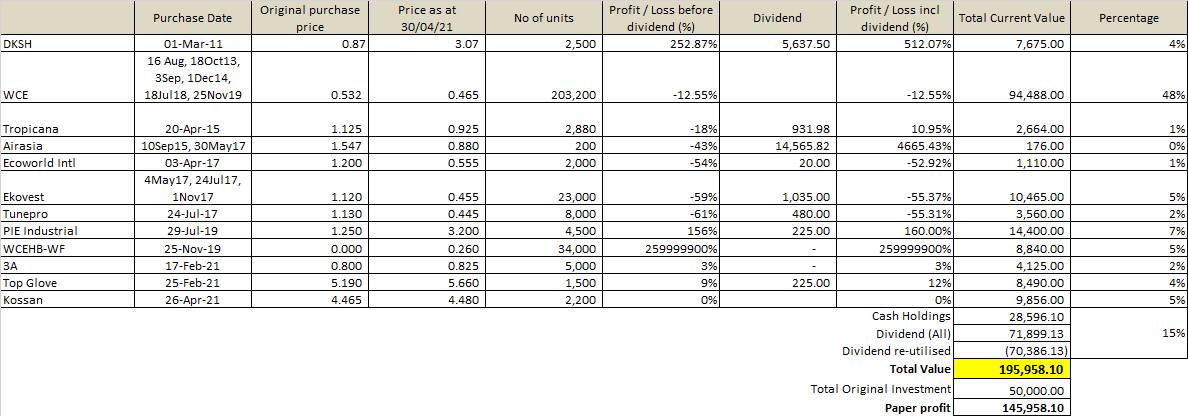

Why I bought Kossan

If we noticed the market nowadays, it has been much more on sentiments rather than being rational. There's a lot more trading activities today where even the large funds are taking part. The emergence of retail players a.k.a. the "Robin Hood"s investors is allowing much more purchases based on sentiments. There are possibly tonnes of Telegram and Youtube groups advising people where and how to invest. When I switched on youtube channels on investments, even Gurmit Singh (Phua Chu Kang) in partnership with a young investor advisor is involved.

With this I would deem that there's opportunities to search for value. The rubber gloves companies do not need any more introduction as there are just too much "noise" out there. On my part I see that although vaccine is on the way and few countries (Israel, UK, maybe US) have shown good progress from the vaccination program, I believe it will take years before COVID will be fully addressed. In the past I was just too optimistic. Even as at now, many countries are seeing fresh highs as people get more agitated due to the length of the pandemic and they just take less precautions.

Even most economies could not bear the brunt of inactivities and they just have to open up. One do not need to look far but at Malaysia. Many governments are taking the stand that they just need to allow economies to work for its money (with conditions).

The first round of MCO, there was money being ditched out to people (Makcik Kiah), Second round there were more funds but lesser amount. Moratorium for loans were introduced and practiced during the first six months. Those have stopped. Now, it is much more targeted assistance and even then they are in small bits and pieces.

I believe those similar situations are being practiced in many other countries which are developing when the virus is still rampant. In India, I was expecting the collapse of the health situation many month ago but it seems that they were contained - possibly because of people were willing to adhere to SOPs - and human beings especially from the democratic block were only willing to adhere to so as much. Now we see the brunt of what COVID can do to a country like India (with 1.3 billion people), poor developing country and with lack of basic discipline.

Hence, COVID is here to stay for a while even with vaccines.

For gloves, there is no doubt there will be more companies starting to produce more. But the demand will still be outstripping supply until to a point when COVID is addressed. Even then, let's think through - with a pandemic this scale, many countries would be looking at relooking at their capacity to address the next pandemic. I do not think gloves will be much oversupplied for a while because of this.

I know that certain countries would be looking at gloves self-sufficiencies at some of point of time but there are just few countries which are manufacturing scale developed - which is why Malaysia is one of the beneficiaries from the gloves manufacturing capabilities.

Due to the above, I have hence bought Kossan (2200 units) for the Felice's Fund.

From 2 months ago until now, I have also sold some 3A and redeemed TA due to its delisting.

As for the latest fund position, it is as below.

Thursday, February 25, 2021

Purchased Top Glove

While in the past, I was critical but unsure of the company, this time around I think it is grossly oversold. The company had not paid much dividend as yet and has been repurchasing a substantial amount of its stocks over the pandemic period. The company remains to be the largest gloves manufacturer and is probably the company that benefitted the most in terms of revenue and profits due to the pandemic.

This is probably due to the aggressive nature of the management where they had increased capacities through organic and acquisition growth. The super abnormal profits have given opportunities I believe for many of the gloves manufacturers to improve on their efficiencies in the long run as they took this period to push more automation as well as improve on the living conditions of their workers especially the foreign workers.

I think given that Top Glove is trading at RM43billion valuation, it could be cheap. Post pandemic which for many countries could be seen by end of this year or mid of next year, we will potentially see restocking as these countries do not want to be shocked again by another similar situation. I think these gloves companies despite the coming on stream of other new entrants as well as much increased capacities of the existing company (including China and Thailand) may still see the plants running at full capacities.

I have hence bought 1500 units of Top Glove at RM5.19.

Thursday, February 18, 2021

Bought Three-A Resources, Sold Freight and latest

I have decided to make some changes on my holdings by first selling all 17,500 units of Freight Management which happens to be a very well managed company. Even then, I felt that the recent rise of logistic companies provided a good enough price for me to sell.

From that sale, I decided to buy 10,000 units of Three-A resources (3A - 0012) as I felt that it has not been much followed by many investors. Typically like the business as it is trading at below 13x PE. So who says that we cannot find value during the time when some sector's valuation have gone very high - technology sector mostly.

Tuesday, February 16, 2021

Two factors which could push DNEX higher

Well, tis the season for speculation. I do not really advise on speculation.

However, when I read some of the exercise regarding DNEX, there are some obvious reasons which somehow things may happen given the volatility.

Purchase price and manner the payment is made to the 60% of owners of Ping Petroleum. DNEX is buying Ping and one portion is paid by cash, another via shares.

Well, I still use the word "could" as anything can happen. Shares can crash. DNEX may find other ways to raise more cash. Ping Petroleum's exercise may not go through. Silterra's deal may not happen. For example.