Frankly, I do not have a good feel of the company. I remember many years ago, MOL Access Portal was delisted because the company was not going anywhere despite it being an online payment system company and it was mainly selling credits at cybercafes for mainly those playing online games.

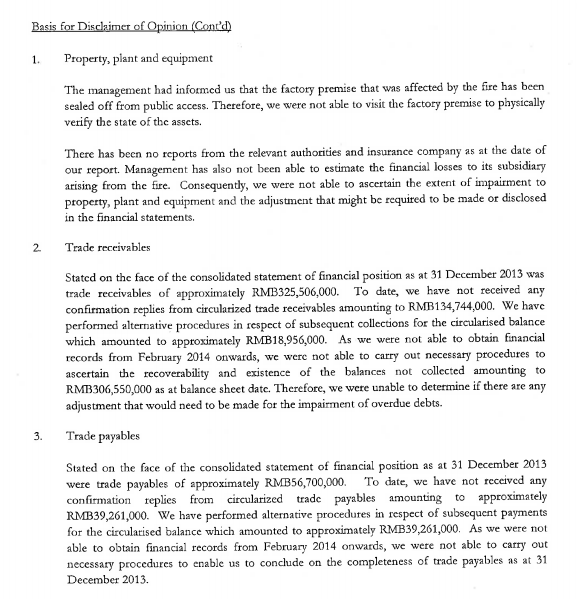

I could not really see and vision how it can grow much. Then few years ago, we hear of it buying Friendster and that was the smart financial dealing when Friendster's patents was used as a negotiation tool for a small portion of Facebook's shares. It must have been worth a lot now i.e. to the tune of at least a billion ringgit now that Facebook is worth USD172 billion (15 Jul 2014).

However news keep on prompting us that MOL Online is doing a hundreds of millions fund raising first locally and over the last few years it seems they have moved to Nasdaq. Frankly, I would have thought this company would have made at least RM50 to more than RM100 million in profits as anything less, it would not be Vincent Tan worth, or at least may not be able to raise that few hundreds of millions. It is not. At last the financial numbers are out with news claiming that it is

raising USD300 million. For it to raise USD300 million, the company must be worth at least USD1.5 to USD2.0 billion as they would probably only release 20% of their shares? Maybe more, I do not know. But let me know from the below numbers, is MOL worth that much?

|

| MOL's last 3 years P&L. Click to enlarge |

In Malaysia, I would not have that buy in, as I do not really have a strong vision of how much growth the company can have. Already, it has been around for many years and online payment company has many competition. The modest operandi to operate this is not to sell through 7-ELeven or any shops but I have always thought the best way is to convert points is through your e-banking systems, ATM machines etc. Hence, I thought the winners would be the banks. If the winners are through the purchases at 7-Elevens and petrol stations, MOL would have made that RM50 million or more profits at least by now. This is because the reach that MOL and through Vincent Tan's retail reach are easy and plenty, especially in Malaysia. Banks would still be the winners as they have the best reach and marketing money. MOL would still be far behind.

Currently, MOL is already operating in many countries - Malaysia, Thailand, Vietnam, Philippines and very recently it bought some operations in Turkey (we Malaysians like Turkey now) and Brazil.

|

| Quarterly income statement for last 8 quarters. Click to enlarge |

If you notice the last 8 quarters results, the main growth was over the last 4 quarters. You see, if I have loads of cash, I can make more cash as through acquisition, I can show that the company and business grows by leaps and bounds but these are not organic growth. See above's image. If the revenue is big for especially businesses with thin margins such as MOL's business, more magic can be squeezed for profits. Why am I seeing that it is starting to make much more profits over the last few quarters when the business has been around for more than 10 years? The cashflow as below may be better reflective of its actual ability, I hope.

|

| Cashflow for last 3 years - Click to enlarge |

If your read below, most of the growth are through acquisition recently i.e. Thailand, Brazil, Turkey etc. Usually, revenue will also increase especially prior to any IPOs.

|

| Click to enlarge |

If these numbers are not that fantastic, how can it be worth more than RM4 billion as it would have been. Well, I am also reading Janet Yellen's remark during her statement to Capitol Hill today, "

In equity markets, the Fed saw signs of increased risk-taking limited to small-cap stocks and biotech and social media shares."

MOL is not under any of that category though, i.e. social media or biotech - maybe it is not risky then?

However, I personally think that the space it is in is hugely competitive. The barrier to entry is huge and it will not be able to compete against many free platforms such as banks platforms, ATMs etc. when they are providing it as a service. In other areas it is competing against the likes of Whatsapp, Wechat etc. No way it can be dominant as this space is hugely convulated.