I am sure many people would be concerned and confused on what to do with WCE which is a toll concession business after the Pakatan Harapan (PH) has won the election. Among the manifesto, PH has proposed for a staged elimination of toll concessions in Malaysia. They are also proposing for renegotiation of the highway concession contracts.

I have seen several press articles as well as a

video put up by Tony Pua.

Well, while some of the toll concession businesses has made tonnes of profits (such as LDP, Maju, PLUS), the way it is presented (by Tony) is somewhat misleading. One cannot just say that because of the concessionaire has invested a "

y" amount of money and they have profited several times more from the

y investment, then the concession should be bought back at cost +.

In finance, where especially projects are concerned, one of most important theory is "Time Value of Money". I do not want to explain so much on that concept, but

here is a good explanation. From that explanation, usually for a project to kickstart especially concession business such as the toll, the concession owner will invest upfront for a number of years (in the case of WCE - more than 5 years), and upon the completion, they will start collecting from the tolling proceeds.

Note that finance is different from accounting. Finance has element of time while accounting does not take into account time. In this case, finance is more relevant.

As in any business, the biggest question is who will be coming up with that big sum of money (including cash and borrowings) and ultimately allowing the government to buyback the projects at cost or even cost plus? Nobody.

It is illogical. Nobody wants to take up that risk that way. It defeats entrepreneuralism.

This is because there are completion risk, borrowing risk and return risk that the business concession has to stomach. As an example again for WCE, there are not many construction companies that can complete these kind of projects. Why it has been delayed is that companies like Talam were not capable of doing it and ultimately not getting the financing and support needed. Hence, me being convinced to invest into this project is because it is a IJM led project. Even then, as one can see, there are additional risks now.

One of the biggest message that has been given by the current PH government is the application of the "rule of law". Mahathir also put huge importance onto the economy (which is why the council of elders comprising of 5 very experience people i.e. Daim, Zeti, Robert Kuok, Hassan Merican and Jomo) are all financial and economic experts. Many other countries, their advisors are mix of security, financial, legal etc. But the first team formed in Malaysia are all finance and economy.

To eliminate tolls, the older projects are those such as PLUS, LDP, and PNB owned Prolintas.

All our large funds such as EPF, PNB (ASM and ASB), KWAP, Khazanah etc. owns large proportions of these projects. Prolintas which owns 6 highways i,e, AKLEH, SUKE, LKSA, SILK, DASH, GCE is wholly owned by PNB.

EPF owns 49% of the biggest highway chain in Malaysia i.e. PLUS while the remaining 51% is owned by Khazanah. PLUS has a

RM23.35 billion sukuk bond which is largely unpaid, probably not even paid principal yet. If the government wants to eliminate toll, it has to find ways to repay this i.e. more than RM23.25 billion bonds. By taking out PLUS, it will impact EPF contributors as well. And Khazanah also, which is under MOF.

As it is, there are a lot of financial issues that the government has to tackle and the main part of them are eliminating GST, continuing with BRIM, bringing back some of the subsidies. Obviously, to look at doing away with tolls, it is a very hard task and not as easy as explained by Tony Pua.

The merits of WCE itself

WCE is an important project. It not only connects the west coast where if one is to take the old Federal roads which is inconvenient, but it also connects ports such as Klang, Penang and Lumut. The road is much flatter and more friendlier to heavy vehicles. These are all the important economic development which has been promoted by many of the PH leaders, chief among them Mahathir, Daim and perhaps even Anwar.

Moreover, which part of Malaysia gave the biggest endorsement to the new government? West coast of Malaysia. I.e. connecting Taiping, Lumut, Tanjong Malim, most parts of Selangor - all which have brought the wins to PH.

In fact, I may not be surprise, the new government is better for WCE as some alignment as it is now is still not finalised, especially Tanjong Karang.

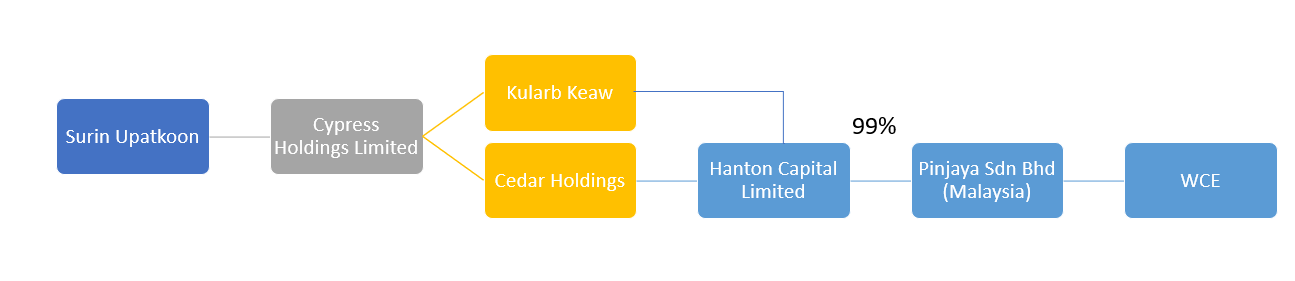

IJM is one of the most respected construction company and without them, the costs of the highway could have been even higher as they are not only capable of building the highway but they are also able to manage the costs.

One should take note that the large part of its management today is from Road Builder Bhd - which was merged into IJM back in 2005. Road Builder as in its name is particularly strong in building roads and West Coast Expressway is not one easy feat. Portions of WCE is on soft soil, which is not easy.

What may happen with the new mandate with the Manifesto

To entirely take away tolls, that is not easy. But to payoff especially the older tolls, that will show that current PH government meant what they promised. The older tolled highways are LDP, Lebuhraya Sungai Besi, first Penang Bridge etc. But even to do that it can be costly as it is not about buying back but also the costs of maintenance.

I would suggest the current PH government to declassify the contracts so that it is becoming more transparent. Speaking of the fairness of the contract, I believe the WCE contract is one of the most fair tolled highways. This is because it has fixed the IRR (actual IRR is not revealed but I hear that it is a higher single digit percentage - not double digit) and if the highway achieves that IRR, government will get a share of the profits over and above the IRR threshold.

I also believe some part of the contracts may be renegotiated. But as mentioned above, a decent IRR (I think) has already been incorporated for the WCE highway.

What about WCE's valuation?

Assuming that the current government is not illogical (by killing the project, and not paying compensation, where even then the court is the remedy for WCE) and follow the rule of law - the price of WCE where it is currently at 93 sen continues to warrant my interest. With the recent proposed fund raising, at 93 sen it will increase the market capitalisation of WCE to RM1.5 billion. This is still a good valuation for investors.

Mahathir has already said the

abolishment of tolls will be done according to the contracts. And the contract mechanism for WCE I believe will have elements of protection for the shareholders. After the contract has been finalised, there were 2 major new shareholders that has gone into the business - MWE and Mamee. They would not have bought into the company if their rights are not protected in the contract.

In summary, the bigger risk after the new government is formed is whether they will follow the "rule of law" as promised and being rational in terms of financial management. Now, let's see!

I have been one of the guys whom have been rooting for a change. That was why I was not concerned with the manifesto of PH especially on tolled highways, but after their big surprise win, it made me think of the consequence of the promise.